|

|||

|

|

|

||

|---|---|---|

|

||

|

||

|

||

|

||

|

||

|

||

|

|

|

|

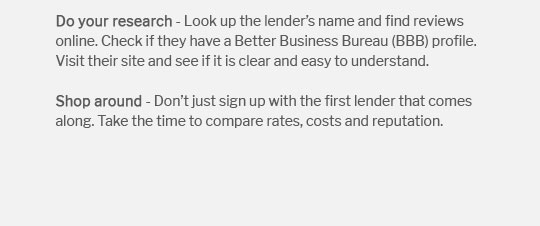

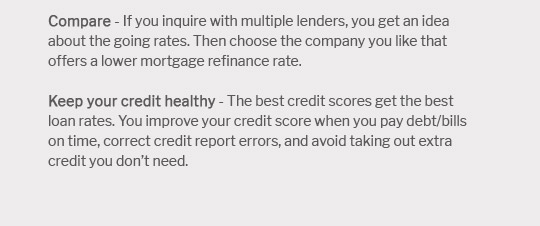

Understanding Mortgage Refinance in Washington State: A Comprehensive GuideRefinancing a mortgage in Washington State can offer homeowners the opportunity to secure better interest rates, reduce monthly payments, or change the term of their loan. This guide will explore the benefits, process, and considerations of mortgage refinancing in the region. What is Mortgage Refinancing?Mortgage refinancing involves replacing an existing mortgage with a new one, usually to obtain more favorable terms. Homeowners in Washington State often consider refinancing to take advantage of lower interest rates or to switch from an adjustable-rate mortgage to a fixed-rate mortgage. Benefits of Refinancing in Washington StateLower Interest RatesOne of the primary reasons homeowners refinance is to take advantage of lower interest rates. This can lead to significant savings over the life of the loan. Change in Loan TermRefinancing allows homeowners to change the term of their loan. For instance, switching from a 30-year to a 15-year mortgage can increase monthly payments but reduce the overall interest paid. Accessing Home EquityRefinancing can also provide access to home equity, which can be used for home improvements or other financial needs. Steps to Refinance Your Mortgage

Considerations Before RefinancingWhile refinancing can offer benefits, it's essential to consider potential drawbacks. These may include closing costs, prepayment penalties, and the impact on your financial situation. Frequently Asked QuestionsWhat are the costs associated with refinancing?Refinancing typically involves closing costs, which can range from 2% to 5% of the loan amount. It's important to weigh these costs against potential savings. Can I refinance my mortgage if I have owned my home for less than a year?Yes, you can refinance your mortgage even if you have owned your home for less than a year. It's crucial to evaluate your financial situation and the fha refinance less than 1 year options available to you. How does refinancing affect my credit score?Refinancing can have a temporary impact on your credit score due to hard inquiries. However, making timely payments on the new loan can help improve your score over time. https://dfi.wa.gov/homeownership/refinancing

People typically refinance their mortgage to lower their interest rate and monthly payments. https://wsecu.org/loans/mortgage-refinance

Mortgage refinancing to reach your goals - Skip to rates - Why refinance your home loan? - Switching lenders is simple - Apply now - Choose a fixed-rate or ... https://www.washsb.com/calculator/mortgagerefinance

Use the mortgage refinance calculator to sort through a multitude of factors including your current interest rate, the new potential rate, closing costs and ...

|

|---|